The Real Math Behind the Carbon Market 2.0

How Marginal Abatement Cost (MAC) Approach Can Unlock real Innovation, Technology Transfer, and Cost Efficiency

Many times over the last 20 years, I’ve asked myself: Why has the carbon market never fully delivered on its promise?

There’s always been this feeling that the next big thing is just around the corner. But for one reason or another, it never quite happens. Hopefully this time is different…

Today, the market is buzzing with two major buzzwords: Article 6 and CORSIA. The promise? That we’re finally building a global carbon market—one that connects countries, channels finance, and creates real demand from many sectors such as aviation . Big volumes. High prices. Everyone happy.

It all sounds exciting. But here’s the real question: Why do we need a carbon market?

The carbon market exists for a simple and essential reason: to allow companies to allocate capital into emissions reductions and removals that are more cost-effective, even if those projects lie outside their own carbon footprint.

We can debate whether this logic is perfect or fair. But one thing is clear: without a well-functioning global carbon market, achieving net zero will be extremely difficult—if not impossible.

In a world of rising geopolitical complexity, many companies are slowing down their climate commitments—or even backtracking on pledges made just a few years ago.

Believing that companies should reduce everything internally first and only use the carbon market “in 20 years” may sound responsible—but in reality, it’s a mistake. We don’t have the luxury of waiting. We need to scale every tool we have, now.

Today, about 24% of global emissions are covered by a carbon price—via taxes or regulated carbon markets. That’s a positive sign. And it’s becoming clear that companies respond far better to compliance signals than to voluntary ones.

CORSIA is a good example: the aviation sector, despite the long process, is beginning to learn how to use high-quality carbon credits—and how to invest in them.

Similarly, Article 6 is increasingly seen as the regulatory bridge to the future. It offers flexibility and the potential to help countries ratchet up their climate ambition. And political momentum is growing, even in places where the door was once shut.

Until recently, the EU was strongly opposed to the use of international credits. But the mood is shifting. Several EU member states, including Germany, are now voicing support for limited integration of Article 6 credits within the EU ETS.

“We recognize that international cooperation under Article 6 can complement domestic action, and we are open to exploring how it can be integrated into our carbon pricing systems in a way that safeguards environmental integrity.”

— German Environment Ministry official, 2024

That’s promising. Carbon markets can bring flexibility and cost efficiency in countries where the marginal carbon abatement cost is high.

But despite the Article 6 rulebook being finalized in Baku this year, we’re still struggling to figure out how to operationalize it.

One major challenge is that—for the first time—governments must authorize the export of credits, triggering a corresponding adjustment to their national inventory. This creates new risks for developers: delays, shifting priorities, or even revocation of authorization.

Most countries aren’t ready. Even those that are more advanced are still asking themselves: Which projects should we authorize—and which should we keep?

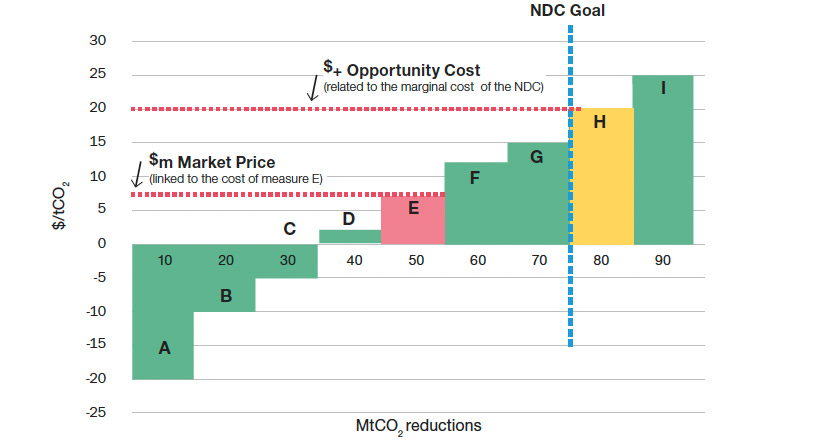

This is where the MAC (Marginal Abatement Cost) approach becomes crucial.

The Marginal Abatement Cost (MAC) curve is a tool used to rank different emission reduction options by their cost per ton of CO₂ reduced. It helps policymakers visualize which actions are the cheapest—and therefore most efficient—to implement first. On the left side of the curve are low-cost measures (like improved cookstoves ), while more expensive interventions (like carbon capture) sit on the right. By aligning project authorizations with the MAC curve, countries can retain the most cost-effective actions for domestic use and offer the higher-cost ones to international markets.

When a country authorizes a carbon project under Article 6, it accepts a liability—it must increase ambition elsewhere to compensate for the exported mitigation.

For example (figure 2), if a country can reduce emissions for $6/ton (activity E) with improved cookstoves, and $20/ton through power grid upgrades (activity H), selling the $6 credits means it will later need to pay $20/ton or more to meet its targets.

In this case, the opportunity cost of selling and transferring can be identified as the cost of the lowest cost mitigation activity going beyond the NDC target, e.g., activity H in figure 2 at a cost of $20/tCO2e. If the MAC curve is correct, the opportunity cost represents the real cost of the corresponding adjustment for the host countries.

In the market, I’ve seen many offers circulating for traditional improved cookstove (ICS) projects backed by Letters of Authorization (LOAs), and I always ask myself: Why would a country authorize its cheapest mitigation option? To me, it makes no sense—economically or strategically. And beyond that, it creates significant risks for investors and buyers, who may ultimately be exposed to projects that should have been retained for domestic NDC compliance.

This concern becomes even more relevant when we consider that the average price in the voluntary carbon market in 2024 was just $6 per ton, according to the latest Ecosystem Marketplace report. That figure reflects a voluntary market heavily skewed toward low-cost mitigation options—those found at the bottom of national MAC curves.

Under Article 6, this creates a potential conflict: if countries authorize and export their cheapest mitigation options, they risk having to achieve the same climate targets later through more expensive domestic actions. That’s why aligning authorizations with the MAC curve—retaining low-cost options domestically suitable to be used in local compliance or in the voluntary market, and exporting high-cost, additional mitigation—is not just good strategy, it’s economic self-preservation.

Don’t get me wrong: the market needs to start and show success with the first transactions. In the short term, countries could start authorizing projects—even with low abatement costs—to test procedures and gain experience. But in the mid-to-long term, they should shift toward prioritizing higher-cost, additional projects that depend on carbon finance to happen.

The MAC approach doesn’t contradict the role of carbon markets in improving cost efficiency—it refines it. At the national level, MAC helps countries protect their least-cost mitigation pathways. At the global level, carbon markets can still deliver efficiency by reallocating finance to where it’s needed most.

But here’s where it gets even more complex. NDCs are updated every five years, and MAC curves shift as technology costs evolve. A project considered “high-cost” and exportable today might be reclassified as “low-cost” tomorrow. That creates major uncertainty.

Developers and buyers face a key risk: If a country updates its MAC priorities, future authorizations or corresponding adjustments could be denied, delayed, or renegotiated.

To manage this, countries and project developers need:

Transparent MAC methodologies and regular updates

Long-term Article 6 strategies aligned with NDC trajectories

Stability clauses in ITMO agreements to protect authorized projects for 5–10 years

Differentiated treatment for projects with high additionality, high cost, or strong co-benefits

Ultimately, predictable and transparent governance will be essential to make Article 6 investable—especially in a world where both climate ambition and national interest are moving targets.

Beyond enabling cost-effective mitigation, the carbon market is evolving into a platform for innovation and technology transfer. We shouldn’t lose sight of a broader opportunity: to incentivize companies to bring breakthrough solutions to emerging economies. Companies with cutting-edge technologies can implement transformative projects in host countries—generating impact while opening new markets. One interesting case is the Japanese carbon market, where projects promoted in host countries must include Japanese corporate and technologies in the projects proponents . This is a strategic way for a government to promote economic growth, internationalization, and cooperation, while driving climate finance.

In this way, the carbon market can serve not only as a climate tool but also as a catalyst for exporting innovation, driving industrial cooperation, and unlocking low-carbon development. By adding a predictable revenue stream through carbon credits, the market can help de-risk pioneering projects, making climate investments more bankable and scalable where they’re most needed.

To answer the question posed at the start of this article: If the carbon market wants to become a global reference point in fighting climate change—not just a promise—it must embrace this dual role. Yes, it should drive economic efficiency. But it must also drive ambition, innovation, and collaboration. Only then will it fulfill its true potential.

Andrea, many thanks, your article offers one of the clearest and most pragmatic explanations of how the carbon market can evolve into a strategic tool for both economic efficiency and climate ambition!

Very useful and interesting analysis. Thanks Andrea!